FIDEUM: Difference between revisions

No edit summary |

No edit summary |

||

| Line 1: | Line 1: | ||

== Finanzderivate in unvollständigen Märkten <br> (Modeling and Valuation of Financial Derivatives in Incomplete Markets) == | == Finanzderivate in unvollständigen Märkten <br> (Modeling and Valuation of Financial Derivatives in Incomplete Markets) == | ||

financed by the BMBF support program: Mathematics for innovations in the Industrial and Service Sectors | |||

'''Brief description'''<br><br> | '''Brief description'''<br><br> | ||

| Line 52: | Line 34: | ||

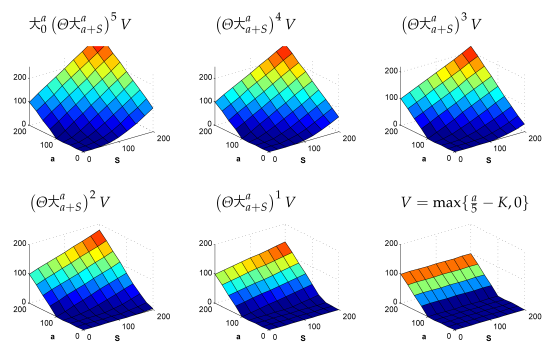

'''Abbildung 2:''' Aus dem Modell wird eine Simulation erzeugt: Hier wird die Entwicklung einer Asiatischen Option abgebildet. | '''Abbildung 2:''' Aus dem Modell wird eine Simulation erzeugt: Hier wird die Entwicklung einer Asiatischen Option abgebildet. | ||

===Kooperationspartner:=== | |||

* Prof. Dr. Drs. h.c. Willi Jäger (IWR, University of Heidelberg) | |||

* Prof. Dr. Markus Reiß (Institute of Applied Mathematics, University of Heidelberg) | |||

* Prof. Dr. Michael Griebel (Institute for Numerical Simulation, University of Bonn) | |||

===Industriepartner:=== | |||

[http://www.thetaris.com http://www5.in.tum.de/wiki/uploads/b/bc/FIDEUM_ThetarisLogo.png] | [http://www.thetaris.com http://www5.in.tum.de/wiki/uploads/b/bc/FIDEUM_ThetarisLogo.png] | ||

===Kontakt:=== | |||

[[Stefanie Schraufstetter]], [[Stefan Zimmer]] | |||

Revision as of 12:47, 2 February 2009

Finanzderivate in unvollständigen Märkten

(Modeling and Valuation of Financial Derivatives in Incomplete Markets)

financed by the BMBF support program: Mathematics for innovations in the Industrial and Service Sectors

Brief description

Incomplete markets require new statistical, analytical, and numerical methods, to cope with stochastic volatilities or jumps in the stochastic processes, e.g. These are investigated in a joint project of Universität Heidelberg (with focus on modeling, analysis and statistics), Universität Bonn (with focus on numerics) and SCCS (with focus on software development). The goal of our work in the project is to integrate newly developed methods - especially sparse grid techniques - into the framework of ThetaML, a system of Thetaris GmbH that allows rapid formulation and analysis of complex financial derivatives.

Finanzderivate in unvollständigen Märkten

Simulationssoftware ist ein notwendiges Werkzeug, um die immer schneller ent wi ckel ten und komplexer werdenden Finanzprodukte verständlich zu machen. Dabei ist die Umsetzung neuer Modelle und effi zienter Verfahren für den Computer entscheidend für die erfolgreiche Anwendung in der Praxis. Die Modellierungssprache verwendet dabei ihr ganz eigenes Vokabular. Kaum hat der Anwender seine Produktbeschreibung in Worte gefasst, wird es automatisch in eine numeri sche Simulation umgewandelt. ThetaML ist ein neu entwickeltes System, das mit einer simplen, jedoch sehr mächtigen Beschreibungssprache arbeitet. Es repräsen tiert zusätzlich eine Plattform für die Implementierung der im Rahmen des Projekts entwickelten Modelle und Methoden

Abbildung 1: Ein Finanzprodukt – hier eine Amerikanische Option – kann graphisch in einem „Thetagram“ oder als Text im so genannten „ThetaScript“ modelliert werden.

Abbildung 2: Aus dem Modell wird eine Simulation erzeugt: Hier wird die Entwicklung einer Asiatischen Option abgebildet.

Kooperationspartner:

- Prof. Dr. Drs. h.c. Willi Jäger (IWR, University of Heidelberg)

- Prof. Dr. Markus Reiß (Institute of Applied Mathematics, University of Heidelberg)

- Prof. Dr. Michael Griebel (Institute for Numerical Simulation, University of Bonn)

Industriepartner: